Introduction:

Electric Bike Insurance is not just for riders anymore. By 2026 they will be a way to get around big cities like Amsterdam, London, and Berlin, as well as newer mobility markets such as Lahore. Lots of people, including commuters, university students, delivery professionals, and travelers who care about the environment, now use electric bikes to get where they need to go.

The truth is:

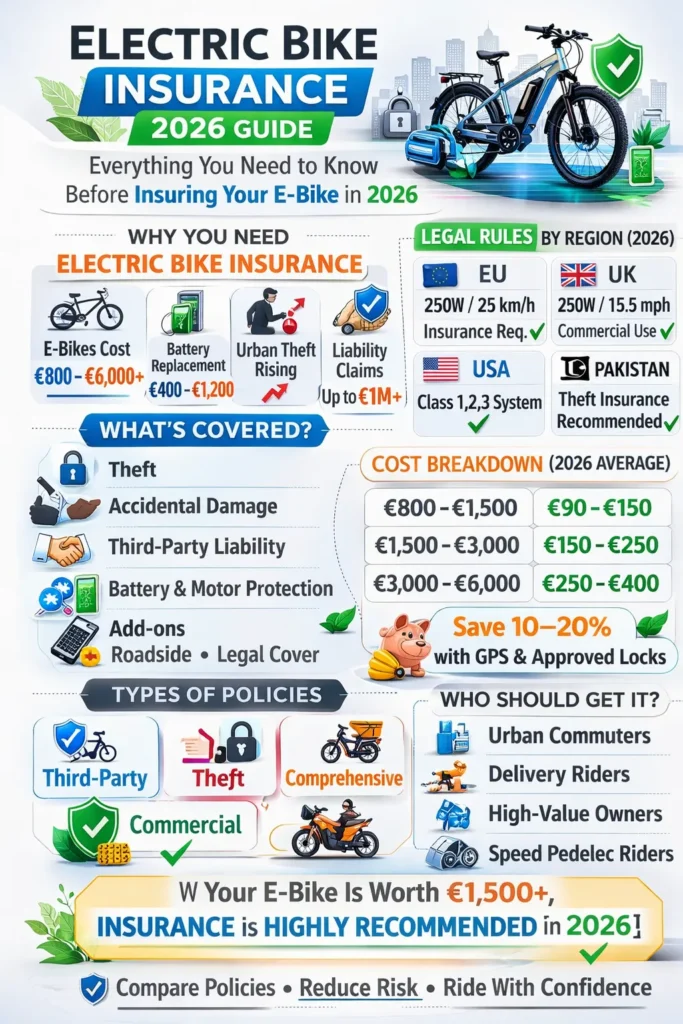

Most e-bikes today cost between 800 euros and 6,000 euros or more. High-end models can easily cost over 7,000 euros. Just the battery can cost between 400 euros and 1,200 euros. Parts like drive motors, digital displays, and hydraulic brakes can make repairs very expensive. At the time, bike theft is going up in big cities, and accidents are getting more complicated.

This is why having insurance for bikes is not just a good idea for many riders. It is a smart way to protect their money.

In this guide, you will learn:

- What electric bike insurance truly means

- Legal requirements in the EU, UK, USA, and Pakistan

- Coverage types explained clearly

- Detailed 2026 cost breakdown

- Advantages and disadvantages

- Side-by-side comparison tables

- Real-world case examples

- Step-by-step buying guide

- Common mistakes to avoid

- Expert verdict for 2026

What Is Electric Bike Insurance?

Electric bike insurance is a specialized protection policy designed specifically for electric bicycles. It provides financial compensation if your e-bike is stolen, damaged, vandalized, or involved in an incident that causes liability.

Unlike standard bicycle policies, electric bike insurance recognizes that e-bikes contain:

- Electric motors

- Lithium-ion battery packs

- Electronic control systems

- Digital displays and sensors

- High-value drivetrain components

These integrated technologies increase both market value and repair complexity. Because of this, standard bicycle insurance policies often provide insufficient coverage.

Electric bike insurance is structured to protect against monetary loss, liability exposure, and unexpected repair bills.

Why Standard Bike Insurance Is Not Enough

Many riders assume:

“My home insurance will cover it.”

Or

“Regular bicycle insurance is sufficient.”

Unfortunately, this assumption is frequently inaccurate.

Problems With Traditional Bicycle Insurance

Standard policies may:

- Exclude electric motors

- Limit battery protection

- Offer lower reimbursement caps

- Refuse coverage for motorized use

- Deny commercial usage claims

Additionally, compensation limits may not reflect the full replacement value of a premium e-bike.

What About Motorcycle Insurance?

Motorcycle insurance is also usually unsuitable. Most pedal-assist e-bikes do not qualify as motorcycles under legal definitions because of limited power output and speed restrictions.

This legal and coverage gap is exactly why electric bike insurance policies were developed.

Do You Legally Need Electric Bike Insurance in 2026?

The requirement depends on:

- Country

- Motor power

- Maximum assisted speed

- Vehicle classification

Let’s examine the main regions.

🇪🇺 European Union – Electric Bike Insurance Rules

The European Union defines most standard e-bikes as EAPCs (Electrically Assisted Pedal Cycles).

Typical criteria:

- Maximum motor power: 250W

- Assistance limit: 25 km/h

- Pedal-assist only (no throttle-only systems)

Under EU transport rules, these standard e-bikes generally do NOT require mandatory insurance.

However, a separate category exists.

Speed Pedelecs (Up to 45 km/h)

Speed pedelecs often:

- Require vehicle registration

- Require insurance coverage

- Require helmets

- Require license plates

In countries such as Germany and Belgium, insurance identification stickers are mandatory for high-speed models.

🇬🇧 United Kingdom – Electric Bike Insurance Laws

In the UK:

- Motor limit: 250W

- Maximum assisted speed: 15.5 mph (25 km/h)

- Pedal-assist only

Standard e-bikes do not legally require insurance.

However:

- Delivery riders typically need commercial coverage

- Speed pedelecs require registration and insurance

Commercial riders face greater liability exposure and should not rely on personal policies.

🇺🇸 United States – 3 Class E-Bike System

The United States uses a three-class system:

| Class | Description | Insurance Required? |

| Class 1 | Pedal assist up to 20 mph | Usually No |

| Class 2 | Throttle + 20 mph | Usually No |

| Class 3 | Pedal assist up to 28 mph | Rarely mandatory |

Insurance requirements vary by state. Riders should consult local Department of Motor Vehicles regulations.

🇵🇰 Pakistan & Emerging Asian Markets

In Pakistan:

- Low-power pedal-assist bikes typically do not require registration

- High-power electric motorcycles may require licensing

- Theft risk is increasing in major cities

In urban centers such as Karachi, theft insurance is strongly recommended due to rising crime statistics.

Why Electric Bike Insurance Is Becoming Essential

Even when not legally required, insurance provides strong financial protection.

Reasons include:

- Rising e-bike price

- Increasing urban theft rates

- Expensive battery replacement

- Growing accident liability claims

- Higher risks for delivery workers

In dense cities like New York City and Paris, theft incidents involving electric bikes have increased significantly in recent years.

Insurance protects not just the bicycle, but your financial stability.

What Does Electric Bike Insurance Cover?

Coverage varies by insurer, but most policies include the following components.

Theft Protection

Covers:

- Theft from Home storage

- Theft from public parking areas

- Forced entry incidents

- In some cases, international theft

Requirements often include:

- Approved high-security lock

- Proof of forced entry

- Police report documentation

Accidental Damage

Covers:

- Crash damage

- Fire damage

- Vandalism

- Natural disasters

If you fall during commuting and damage your motor or frame, comprehensive insurance typically covers repair or replacement costs.

Third-Party Liability

This is one of the most important protections.

Covers:

- Injury to pedestrians

- Damage to vehicles

- Property damage

- Legal defense costs

In Europe, liability limits commonly range from €1 million to €5 million.

Without liability insurance, a serious accident could lead to devastating legal expenses.

Battery & Motor Coverage

This is a defining feature of electric bike insurance.

Lithium-ion battery packs are expensive and sensitive to damage. Premium plans may cover:

- Battery theft

- Electrical faults

- Motor malfunction

- Controller replacement

However, wear and tear is usually excluded.

Add-Ons and Extra Protection

Optional benefits may include:

- Roadside assistance

- Legal expenses coverage

- Personal accident compensation

- Worldwide travel protection

- Accessory coverage

Types of Electric Bike Insurance Policies

| Coverage Type | Theft | Damage | Liability | Battery | Best For |

| Third-Party Only | ❌ | ❌ | ✅ | ❌ | Legal minimum |

| Theft Only | ✅ | ❌ | ❌ | Sometimes | Urban riders |

| Comprehensive | ✅ | ✅ | ✅ | ✅ | High-value e-bikes |

| Commercial | ✅ | ✅ | ✅ | ✅ | Delivery riders |

Comprehensive policies provide the broadest safeguards.

How Much Does Electric Bike Insurance Cost in 2026?

Premiums depend on multiple variables.

Average Annual Premiums (Europe 2026)

| Bike Value | Basic Theft | Comprehensive |

| €800–€1,500 | €30–€80 | €90–€150 |

| €1,500–€3,000 | €70–€150 | €150–€250 |

| €3,000–€6,000 | €120–€250 | €250–€400 |

Cost Determinants

Insurance providers evaluate:

- Bike valuation

- Local crime statistics

- Rider age

- Storage method

- Claim history

- Security devices

- Commercial usage

Urban residents generally pay higher premiums than rural riders.

How to Reduce Your Electric Bike Insurance Premium

You can lower your annual payment by:

- Using certified high-security locks

- Storing your bike indoors

- Installing a GPS tracking device

- Choosing a higher deductible

- Comparing multiple insurers

- Avoiding unnecessary optional coverage

Small adjustments can reduce premiums by 10–20%.

Electric Bike Insurance vs Home Insurance

| Feature | Home Insurance | E-Bike Insurance |

| Theft at home | Usually Yes | Yes |

| Theft outside home | Limited | Yes |

| Crash damage | Rare | Yes |

| Liability cover | Limited | Yes |

| Battery protection | Rare | Yes |

Home insurance often excludes:

- Motorized components

- High-value claims

- Commercial use

Specialized insurance is more comprehensive and tailored.

Pros & Cons of Electric Bike Insurance

Advantages

- Protects high-value investment

- Covers Battery and motor

- Provides liability security

- Covers theft in public areas

- Required for speed pedeles

Disadvantages

- Annual premium cost

- Strict lock requirements

- Policy exclusions

- Claims paperwork

For most riders, benefits outweigh drawbacks.

Top Myths About Electric Bike Insurance

Myth 1: “My home insurance covers everything.”

It often excludes theft outside the home and motorized components.

Myth 2: “Low-speed bikes don’t need insurance.”

Legal requirements differ from financial prudence.

Myth 3: “Cheap bikes don’t need insurance.”

Even €1,000 is a substantial loss for many households.

Choose the Best Electric Bike Insurance

Step 1: Know Your Bike’s True Value

Include:

- Accessories

- Upgrades

- Battery replacement cost

- Installation expenses

Step 2: Assess Your Risk Profile

Ask:

- Do I park in public frequently?

- Is my city high-risk for theft?

- Do I commute daily in traffic?

- Do I use it commercially?

Step 3: Compare Policies Thoroughly

Evaluate:

- Liability limits

- Battery inclusion

- Deductible amount

- Claim settlement time

- Geographic coverage

Step 4: Review Exclusions Carefully

Common exclusions include:

- Unlocked bicycle

- Racing

- Unauthorized modifications

- Wear and tear

Who Should Definitely Get Electric Bike Insurance?

- Owners of bikes worth €1,500+

- Delivery riders

- Urban commuters

- Speed pedelec riders

- International touring cyclists

If your e-bike is essential for daily mobility, insurance is strongly advised.

Real-World Example

Imagine you own a €2,800 trekking e-bike in Berlin.

- Battery cost: €700

- Theft risk: High

- Annual premium: €180

If stolen, insurance reimburses replacement (minus deductible).

Without insurance, you lose €2,800 outright.

Electric Bike Insurance for Delivery Riders

Delivery professionals face:

- Extended riding hours

- Higher accident probability

- Public parking exposure

- Commercial liability

Standard personal insurance often rejects business-related claims. Commercial electric bike insurance is necessary and includes:

- Business liability

- Higher compensation limits

- Work-related injury coverage

Electric Bike Insurance for High-Speed Models

Speed pedelecs (45 km/h) frequently require:

- Registration

- Insurance plate

- Helmet

- License

These models are often legally classified closer to mopeds, making insurance mandatory in many jurisdictions.

FAQs

A:Only for certain high-speed models in some countries.

A:Only if you choose commercial coverage.

A:But proof of purchase is required.

A:Usually, no wear and tear is excluded.

A:Not mandatory, but it often reduces premiums.

Final Verdict

In 2026, electric mobility is accelerating worldwide. E-bikes are more sophisticated, more valuable, and more integrated into daily transportation systems than ever before.

If your electric bicycle exceeds €1,500 in value, insurance is highly recommended.

Rising theft rates, expensive lithium-ion battery systems, and increasing liability risks make electric bike insurance a prudent and forward-thinking investment.

It provides:

- Financial protection

- Legal security

- Long-term peace of mind

- Investment preservation

Serious riders protect their ride.

Electric bike insurance in 2026 is not just about replacing stolen equipment — it is about safeguarding your mobility, your money, and your Future.